Reusing construction-demolition waste, the technology way: Goutham Reddy

23 Nov 2020

8 Min Read

Editorial Team

Currently, only 1% of C&D waste in India is processed, but that is changing. REEL is one of the largest

waste-to-energy companies in Asia, with over 50% market share of India’s 87 MW installed capacity,

generated by processing 6 million tonnes of waste every year, with waste-to-energy plants in Delhi (24

MW) and Hyderabad. In November 2020, the company partnered with Greater Hyderabad Municipal

Corporation (GHMC) in building a new construction-and-demolition (C&D) waste recycling plant. The

new C&D plant converts 95% of waste back into building material

CW: Today I have the pleasure of Mr Goutham Reddy’s company in a videochat with CW. Hyderabad has

particularly gained a lot from REEL’s expertise. We are hearing more and more about C&D now. What is

a C&D plant?

Goutham Reddy: There are different kinds of waste in the society—municipal or domestic, biomedical,

hazardous, electronic, nuclear, and so on. One of the other kinds of waste that has historically been

neglected is construction-demolition waste. In the process of both construction and demolition, a lot of

excavation waste from construction and debris from demolition are generated. All this waste gets

dumped in available open spaces like parks and playgrounds, and essentially comes in a motorists’ or

pedestrians’ pathway. Such waste may not smell, nor is it hazardous. But it is public nuisance, occupying

large amounts of space and distracting traffic.

The hierarchy and the three pillars of environment management are Reduce – Reuse – Recycle. If

reduction is not possible, we reuse, and where reuse is not possible, we must recycle. Disposal happens

if none of the three processes are possible. Can we get C&D waste into this circular economy? That was

our research. The government, with whom we had discussions, wanted us to help them, and the result

of an agreement between us is this 500 tonne per day C&D plant in Hyderabad. That’s about 25% of the

approximately 2,000 tonnes of C&D waste that Hyderabad generates.

Once we process this waste, it is converted back into building materials. The beauty of this project is that

we can recover up to 95% of the waste—so, this plant gives back 470 tonnes of construction material, in

the form of sand, aggregates, or building blocks.

That is one of the most satisfying parts of this project.

We have now been awarded another 500 tonne plant in Hyderabad, which will be commissioned by

January [2021]. Together, then, these plants will solve half of the city’s C&D waste problem.

CW: Only 1% of C&D waste in India gets recycled. Does that figure surprise you—especially in relation to

how it works internationally, in your observation?

GR: You are right. In many countries abroad such as Singapore, Australia, the United States, and so on,

construction material is of a different nature. There is a lot of wood and fibrous material. In India, 90%

of the waste is cement aggregates.

This means that the technology [for waste processing in India] had to be developed indigenously. We

had to invest a lot of time and research into understanding what the right solution is. We have brought

in seeps, shredders, ballistic separation, liquid separation, and grinding. In combination, we are able to

recover 95% of the waste. I don’t believe that they have achieved this [degree of recovery] in any part of

the world. This is a wonderful achievement for the country.

The 1% rate of recovery of C&D waste is not surprising, because the research is recent. I’d actually say

the research is ongoing as we execute the project, and we will have better-quality products. But the

quality of sand we’re generating is already better than river sand. So is the case with aggregates and

tiles—the product quality is better than virgin products.

CW: In general, what is the difference you find that makes your [waste processing] more efficient

internationally?

GR: For sure, developed economies are more efficient. The collection, transport and disposal

mechanism has become extremely streamlined. Every resident knows the schedule of collection, for

example. This has become a culture and a systematic process that has developed over a period of time.

India has not developed [this culture]. But apart from being systematic, educated and aware, it is a

function of paying capacity.

In the US, the average net cost per tonne that the government or the resident pays is about $250 per

tonne. In India, whether it is municipalities or residents or commercial establishments, even a payment of

Rs 2,000 is considered extremely high. That is why 90% of the municipalities in India don’t pay. And in

turn, that is why we are not getting as many projects as we should. So the change in mindset to a

“polluter pays” principle—and paying for better quality—hasn’t sunk in.

CW: You operate on public-private partnership (PPP). Do you find it necessary to go that route because

many cities still don’t find it profitable [to pay]? What is your revenue model?

GR: The revenue model is two-pronged. First, we charge the municipalities for collection, transport and

disposal. The charge, called tipping fee, varies, typically between Rs 500 and Rs 800 per tonne. Second,

through proceeds of the sale of finished products generated from the waste recycling. We sell the sand,

aggregates and building blocks at market prices. To promote these products, we sell them at prices that

is 10%-15% lower than those of the virgin counterparts of those products—although the quality is

better.

CW: What top lines and bottom lines are you generating?

GR: REEL operates about 65 different plants, of which 20 are biomedical or hospital waste management

facilities, 18 are industrial hazardous waste management plants, another 20 are municipal solid waste

facilities, and about 10-12 recycling plants across different technologies like C&D, plastic, paper, solvent,

and electronics, handling about 6 million tonnes of waste every year—by far the largest in India and one

of the largest in Asia. We generate revenues of about Rs 3,000 crore.

CW: What is the overall recovery rate from waste (since your revenues in a PPP model would largely

depend on that rate)?

Yesterday, we inaugurated another waste-to-energy (WTE) plant in Hyderabad. With this, the total

installed capacity in India is about 87 MW, of which 44 MW is built and operated by us. These are high-

capex plants—up to Rs 25 crore per MW on average. China has 500 WTE plants that generate 4,000-

5,000 MW. India, currently at less than 100 MW, will have no choice but to reach that level. WTE as a

technology has emerged quite well, with good reciprocating grid and gas-cleaning technologies.

The tipping fee for waste management in India is between Rs 2,000 and Rs 3,000 per tonne, depending

on the size of the municipality. Once the waste is received, multiple products including organic manure

(compost), plastic, paper, refuse-derived fuel (sold to cement factories used in boilers as fuel). The

offtake of fuel is not commensurate with its generation—we are not able to get adequate offtake of the

generated fuel from cement industries or boilers.

Therefore, we have started establishing our own WTE plants. These plants are high on capex but good on

technology, probably state-of-the-art. About 400-500 such plants are sure to come up in the country.

They reduce volume by 10% and convert it into energy. That technology is simple—you burn the waste

at high temperature through boiler tubes, inside which water gets converted into steam, after which the

steam turbine converts it into electrical energy. The residual gases are cleaned. But because we are

handling heterogeneous material, the engineering is challenging—hence the high capex.

CW: Are logistics a challenge, both upstream and downstream? Dealing with local contractors, that sort

of thing—do you work in collaboration?

GR: BY virtue of handling 6 mt of collection and transport of waste, we have also emerged as one of the

large transport contractors in the country. We ourselves own a fleet of about 2,000 trucks in different

parts of India. So logistics is a big challenge in India, and as you would notice, we operate in compliance

with the laws—closed containers, compacted waste transport, and ensuring that no spillage happens.

But in India even today, most of the waste happens in very unhygienic open tippers, spilling waste and

releasing stench throughout the drive. Our intention is to change the process to a modern transport

system with tailgate compactors as you would see in the US, UK, and Europe. There waste lies in

completely closed containers—you can walk right next to a garbage truck.

Currently, only 1% of C&D waste in India is processed, but that is changing. REEL is one of the largest

waste-to-energy companies in Asia, with over 50% market share of India’s 87 MW installed capacity,

generated by processing 6 million tonnes of waste every year, with waste-to-energy plants in Delhi (24

MW) and Hyderabad. In November 2020, the company partnered with Greater Hyderabad Municipal

Corporation (GHMC) in building a new construction-and-demolition (C&D) waste recycling plant. The

new C&D plant converts 95% of waste back into building material

CW: Today I have the pleasure of Mr Goutham Reddy’s company in a videochat with CW. Hyderabad has

particularly gained a lot from REEL’s expertise. We are hearing more and more about C&D now. What is

a C&D plant?

Goutham Reddy: There are different kinds of waste in the society—municipal or domestic, biomedical,

hazardous, electronic, nuclear, and so on. One of the other kinds of waste that has historically been

neglected is construction-demolition waste. In the process of both construction and demolition, a lot of

excavation waste from construction and debris from demolition are generated. All this waste gets

dumped in available open spaces like parks and playgrounds, and essentially comes in a motorists’ or

pedestrians’ pathway. Such waste may not smell, nor is it hazardous. But it is public nuisance, occupying

large amounts of space and distracting traffic.

The hierarchy and the three pillars of environment management are Reduce – Reuse – Recycle. If

reduction is not possible, we reuse, and where reuse is not possible, we must recycle. Disposal happens

if none of the three processes are possible. Can we get C&D waste into this circular economy? That was

our research. The government, with whom we had discussions, wanted us to help them, and the result

of an agreement between us is this 500 tonne per day C&D plant in Hyderabad. That’s about 25% of the

approximately 2,000 tonnes of C&D waste that Hyderabad generates.

Once we process this waste, it is converted back into building materials. The beauty of this project is that

we can recover up to 95% of the waste—so, this plant gives back 470 tonnes of construction material, in

the form of sand, aggregates, or building blocks.

That is one of the most satisfying parts of this project.

We have now been awarded another 500 tonne plant in Hyderabad, which will be commissioned by

January [2021]. Together, then, these plants will solve half of the city’s C&D waste problem.

CW: Only 1% of C&D waste in India gets recycled. Does that figure surprise you—especially in relation to

how it works internationally, in your observation?

GR: You are right. In many countries abroad such as Singapore, Australia, the United States, and so on,

construction material is of a different nature. There is a lot of wood and fibrous material. In India, 90%

of the waste is cement aggregates.

This means that the technology [for waste processing in India] had to be developed indigenously. We

had to invest a lot of time and research into understanding what the right solution is. We have brought

in seeps, shredders, ballistic separation, liquid separation, and grinding. In combination, we are able to

recover 95% of the waste. I don’t believe that they have achieved this [degree of recovery] in any part of

the world. This is a wonderful achievement for the country.

The 1% rate of recovery of C&D waste is not surprising, because the research is recent. I’d actually say

the research is ongoing as we execute the project, and we will have better-quality products. But the

quality of sand we’re generating is already better than river sand. So is the case with aggregates and

tiles—the product quality is better than virgin products.

CW: In general, what is the difference you find that makes your [waste processing] more efficient

internationally?

GR: For sure, developed economies are more efficient. The collection, transport and disposal

mechanism has become extremely streamlined. Every resident knows the schedule of collection, for

example. This has become a culture and a systematic process that has developed over a period of time.

India has not developed [this culture]. But apart from being systematic, educated and aware, it is a

function of paying capacity.

In the US, the average net cost per tonne that the government or the resident pays is about $250 per

tonne. In India, whether it is municipalities or residents or commercial establishments, even a payment of

Rs 2,000 is considered extremely high. That is why 90% of the municipalities in India don’t pay. And in

turn, that is why we are not getting as many projects as we should. So the change in mindset to a

“polluter pays” principle—and paying for better quality—hasn’t sunk in.

CW: You operate on public-private partnership (PPP). Do you find it necessary to go that route because

many cities still don’t find it profitable [to pay]? What is your revenue model?

GR: The revenue model is two-pronged. First, we charge the municipalities for collection, transport and

disposal. The charge, called tipping fee, varies, typically between Rs 500 and Rs 800 per tonne. Second,

through proceeds of the sale of finished products generated from the waste recycling. We sell the sand,

aggregates and building blocks at market prices. To promote these products, we sell them at prices that

is 10%-15% lower than those of the virgin counterparts of those products—although the quality is

better.

CW: What top lines and bottom lines are you generating?

GR: REEL operates about 65 different plants, of which 20 are biomedical or hospital waste management

facilities, 18 are industrial hazardous waste management plants, another 20 are municipal solid waste

facilities, and about 10-12 recycling plants across different technologies like C&D, plastic, paper, solvent,

and electronics, handling about 6 million tonnes of waste every year—by far the largest in India and one

of the largest in Asia. We generate revenues of about Rs 3,000 crore.

CW: What is the overall recovery rate from waste (since your revenues in a PPP model would largely

depend on that rate)?

Yesterday, we inaugurated another waste-to-energy (WTE) plant in Hyderabad. With this, the total

installed capacity in India is about 87 MW, of which 44 MW is built and operated by us. These are high-

capex plants—up to Rs 25 crore per MW on average. China has 500 WTE plants that generate 4,000-

5,000 MW. India, currently at less than 100 MW, will have no choice but to reach that level. WTE as a

technology has emerged quite well, with good reciprocating grid and gas-cleaning technologies.

The tipping fee for waste management in India is between Rs 2,000 and Rs 3,000 per tonne, depending

on the size of the municipality. Once the waste is received, multiple products including organic manure

(compost), plastic, paper, refuse-derived fuel (sold to cement factories used in boilers as fuel). The

offtake of fuel is not commensurate with its generation—we are not able to get adequate offtake of the

generated fuel from cement industries or boilers.

Therefore, we have started establishing our own WTE plants. These plants are high on capex but good on

technology, probably state-of-the-art. About 400-500 such plants are sure to come up in the country.

They reduce volume by 10% and convert it into energy. That technology is simple—you burn the waste

at high temperature through boiler tubes, inside which water gets converted into steam, after which the

steam turbine converts it into electrical energy. The residual gases are cleaned. But because we are

handling heterogeneous material, the engineering is challenging—hence the high capex.

CW: Are logistics a challenge, both upstream and downstream? Dealing with local contractors, that sort

of thing—do you work in collaboration?

GR: BY virtue of handling 6 mt of collection and transport of waste, we have also emerged as one of the

large transport contractors in the country. We ourselves own a fleet of about 2,000 trucks in different

parts of India. So logistics is a big challenge in India, and as you would notice, we operate in compliance

with the laws—closed containers, compacted waste transport, and ensuring that no spillage happens.

But in India even today, most of the waste happens in very unhygienic open tippers, spilling waste and

releasing stench throughout the drive. Our intention is to change the process to a modern transport

system with tailgate compactors as you would see in the US, UK, and Europe. There waste lies in

completely closed containers—you can walk right next to a garbage truck.Also read: Urgent need for painstaking management of C&D waste

Haworth India Hosts Women’s Leadership Panel Series

Haworth India marked International Women’s Day by hosting a leadership roundtable series titled ‘Give to Gain’, bringing together senior women leaders from architecture and design firms, corporates and project management consultancies.

The series has been conducted in Delhi and Mumbai, with upcoming sessions scheduled in Bengaluru and Hyderabad on 27 March 2026. Structured as moderated panel discussions followed by audience interaction, the initiative examined the business impact of women’s leadership and the role of inclusive workplaces in supporting professional growth.

Manish Khan..

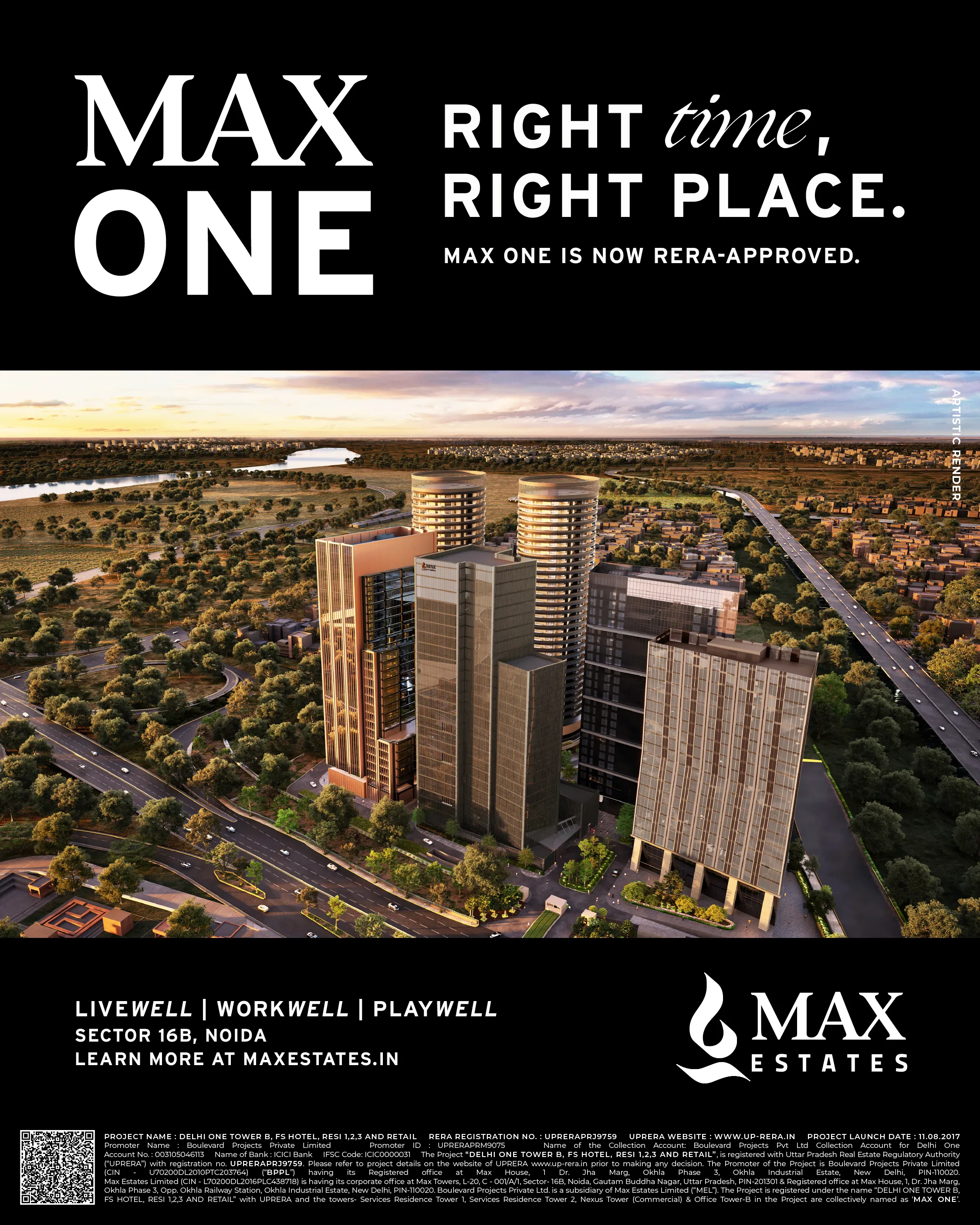

Max Estates has secured RERA approval (UPRERA No.: UPRERAPRJ9759) for its Max One development around Max Towers in Sector 16B, Noida, bringing renewed progress to a project previously stalled following the insolvency of its earlier developer.

Spread across around 10 acres with an estimated development potential of about 2.5 million sq ft, Max One is planned as an integrated mixed-use campus combining serviced residences, premium offices, retail spaces and a private club. The project is expected to generate total sales potential of about Rs 20 billion along with an estimated annuity rental inc..

Hindware has introduced the Starc Smart Wall-Mount Toilet under its Hindware Italian Collection, designed to combine automation, hygiene and contemporary bathroom aesthetics.

The model features automatic flushing, sensor-based seat opening and closing, and remote-controlled functions. It also includes an oscillating water spray and warm air dryer for cleaning, along with a self-cleaning nozzle designed to maintain hygiene.

Additional features include adjustable heated seating, customisable water temperature and pressure settings, a foot-touch flush system and an LCD control interface. The wa..