Shiva Rajaraman, CEO of NIIF IFL, discusses the changes in the infrastructure landscape in the country, policy back-ups and different sources of infrastructure finance that have opened up in the country. With a balance sheet of an impressive Rs.210 billion with zero per cent NPAs, NIIF IFL is an infrastructure debt fund (IDF) that provides innovative and sustainable financing to infrastructure projects in the country.

What are the sources of infrastructure finance in India? What is the sector-wise break-up of your portfolio?

These are Market Size and players. Let me first provide a context to the discussion in terms of size of the market in India for infrastructure finance. India’s GDP is around $3,800 billion. Infrastructure spending in India (including private sector/Public Private Partnership projects and government spending), is around

6 per cent of the GDP, i.e., $230 billion. Out of this, private sector/ PPP projects are our focus area, which is around 25 per cent i.e., $60 billion.

Further, within the debt platform of NIIF, we (i.e. NIIF IFL) fund only the debt portion and not the equity portion (our majority owner

NIIF provides equity) of infrastructure projects. The debt portion (assuming a 70:30 debt equity ratio, on an average, out of the $60 billion referred to earlier) is around $40 billion. Out of that, project companies can take financing from abroad in foreign currency as well as domestically, in Indian rupee. The domestic component is around 80 per cent - roughly

$32 billion. This would translate to around Rs.260 trillion incremental infrastructure rupee debt funding in India in FY 2024. We expect to provide financing to 45-50 projects each year, with an overall market share of between 3-4 per cent, i.e. Rs.80 to100 billion. Our ticket size i.e. lending per project is in the range Rs.1–8 billion, with the incremental average being Rs.2-2.5 billion.

Players:

The aforementioned incremental rupee debt (i.e. market size) for infrastructure of Rs.260 trillion per year is provided by several categories of financiers including banks (private sector, public sector and foreign banks), NBFCs like Power Finance Corporation (PFC), REC, as well as private sector entities like Tata Cleantech, Aditya Birla Finance etc. Other infrastructure debt funds (IDFs) and some insurers such as LIC and a few mutual funds are also active in the area, as are some alternative investment funds (AIFs) registered with SEBI. Based on the above, there are about 25-26 serious players / competitors. There have been some institutions like IDFC Bank that have left this space; there are also new ones that have entered this space.

The latest entrant is the newly created financial institution called National Bank for Financing Infrastructure & Development (NaBFID).

What is NIIF IFL’s rank in infra financing in India?

Today NIIF IFL has a balance sheet size of about Rs.210 billion. In Q1 FY 24, as well as in FY 2023, NIIF IFL has ranked number seven in the country as far as incremental growth of infrastructure loan book is concerned.

Our category of financiers (i.e. infrastructure debt funds set up as NBFCs), are allowed to fund only operational projects, our competitors (i.e. banks, other NBFCs, insurers etc) are allowed to fund under-construction projects as well.

What is NIIF IFL’s portfolio break-up sector-wise?

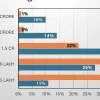

We have consciously focussed on green infrastructure, primarily solar, wind and to a smaller extent, small hydropower projects. About 50 per cent of our portfolio is in solar power generation projects and wind energy projects constitute about 12 per cent. We have not considered large hydropower projects because of their environmental implications. Small hydropower projects constitute 3 per cent of our portfolio. Overall, we have around 65 per cent of our portfolio, in green infra.

The balance 35 per cent portfolio consists of lending to the following sectors:

- Transportation sector (i.e., including roads and airports) around10 per cent,

- Logistics (including like warehousing)

around 8 per cent,

- Communication (including telecom towers) around 7 per cent,

- Power transmission around 4 per cent,

- 4-5 other sectors put together around

6 per cent.

Has the development of the bond market and recent regulatory changes, helped push infrastructure financing?

The development of the bond market in the context of infrastructure, has been slower than expected, but positive. NIIF IFL borrows only through the issuance of bonds and therefore this market is very important for us.

The quality i.e. credit rating of bonds issued and the quality of issuers, both have improved significantly in the last few years. So, the average quality of issuances is now A+, as against BBB four to five years ago, based on publicly available data from rating agencies like CRISIL. The tenor of bonds has also improved. Earlier you had very short tenor issuances. Now, because of demand for long-term bonds from pension, provident and insurance funds, there have been significant higher quality issuances with tenors ranging from 5 to10 years.

Liquidity/trading is also a critical parameter which determines the extent of development of the bond market. Trading has seen some improvement because of various initiatives

by regulators. For example, SEBI mandated that a certain percentage of all funds raised by specified category of corporates, has to be through the issuance of bonds.

Despite some improvement in the liquidity in the bond market, it is still low. The trading in bonds, especially those that are rated below AA+, is low. More bond investors will come in only with more trading. If an investor wants to sell off a bond, he should be able to find

a buyer. Today, this would be difficult, especially for longer tenor infrastructure issuances. Therefore, in this respect, there is significant scope for improvement. There are still relatively few infrastructure-related issuances in the

bond market.

There are various suggestions that have been put forward by the government/regulators and market participants. One has been with respect to the introduction of a category of market makers i.e., institutions that provide buy-sell quotes and help develop both demand and supply. Other suggestions include rationalisation of stamp duty, thereby reducing the transaction cost in such a way that it makes it more economical to both sides. Third is to have measures to encourage large institutions such as Employees Provident Fund Organisation (EPFO) to participate more widely in investment in high-quality private sector issuances. After the IL&FS crisis, institutions such as EPFO have been wary of investing in bonds issued by private sector entities. If such institutions could be mandated to invest in at least the better corporates and higher rated issuances, it could trigger buying and selling of bonds, thereby enhancing liquidity.

In the context of IDF NBFCs, a lot of changes were spelt out in the Reserve Bank of India (RBI) governor’s speech on August 8, 2023, addressing policies and regulation issues that we had been taking to the government and the RBI. Infra debt funds were earlier permitted to fund only

BOT projects. Now all categories of roads projects have been opened up, including Toll-Operate-Transfer (TOT). On the liabilities side, RBI has now permitted us access to external commercial borrowing (ECB). Today we can raise money from international financial institutions, for example, International Finance Corporation (IFC), an arm of the World Bank, Asian Development Bank (ADB), FMO (development bank owned by the Government of Netherlands) or any similar institution, through ECB loans or bonds, which may be utilised for infrastructure, more specifically green purposes. These were not allowed earlier. A third major change is that the regulators have opened the setting up of infrastructure debt funds (IDFs), to various entities with experience, subject to RBI approval. With this more infra debt funds may come up. This could mean more competition for us, but my take is that the market is big enough to accommodate many other players.

What is the difference in risks in lending to different sectors?

The broad heads under which we assess risk are - promoter risk, regulatory risk, market risk, financial risk, technology risk, financing risk, construction risk, operations risk, resource risk and security risk.

For example, market risk could consist of assessment of demand-supply, pricing, quality of off-takers (i.e. counterparty risk), quality of output etc. In projects that we finance, there is no construction risk as we are permitted to provide funding only at the operational stage. Resource risk in wind power projects, for example, would include assessment of wind availability, wind intensity and wind speeds, resource risk for solar power projects could include assessment of the extent of irradiation (i.e. receipt of sunlight on the surface of solar panels), resource risk for “run of the river” hydro power projects, could include assessment of rainfall availability. In the context of security risk, we look at availability of security, charge to lenders and enforceability.

In respect of promoter risk, we must be the only organisation in India that has a formal framework of grading promoter groups (example – G1, G2, G3 etc). Based on this grading, we decide how much we want to lend to the group. The RBI permits a certain percentage of net worth that can be provided as loans to a single promoter group. We do not lend right up to the limit, to every group, rather we lend up to whatever our grading framework mandates us.

In the context of counterparty risk, we have a grading system to assess off-takers like discoms (power distribution entities owned by state governments). Our liquidity buffers (called debt service reserves) are sized based on this grading. We also refer to external ratings of off-takers by CRISIL, PFC etc.

We provide non-recourse financing to “ring-fenced” projects. For example, if ABC group collapses (like IL&FS group collapsed a few years back), our project would remain unaffected because we depend principally on the cash flows of the project and not on undertakings, guarantees etc of payment by the promoter. Our financing is structured in such a manner that we are not dependent on the promoter group at all.

What does a promoter group bring to any infra project? - A promoter (i) acquires land, (ii) secures approvals, permissions etc from the government (iii) brings his share of equity into the project and (iv) gets the construction completed (v) undertakes operation & maintenance (O&M) of the project.

Since NIIF IFL comes in only into the operating stage of a project, risk factors (i), (ii), (iii) and (iv) are already mitigated. The only point on which we are dependent on the promoter group, is in respect of O&M of the project. We have insulated our company from this risk also, by having a contractual right to replace the O&M operator with an O&M operator of our choice if certain parameters are not met, which we check on a periodic basis.

Apart from that, for example in solar power projects, we are the only lender in India who gets solar modules tested under lab conditions to assess degradation over the next few years. The output of this lab report is what we use in

our financial model for making long-term financial projections.

We have a graded system of liquidity buffers - this includes funds set aside in case of any eventuality so that there are no delays in payment of principal and interest to us from the borrower, in any unforeseen eventuality. For example, during Covid, toll booths for road/ highway projects were shut and there was no toll collection. We have a six-month debt service amount, set aside from project cash flows and kept in a separate fixed deposit or in a mutual fund, so that under such eventualities, we (as a lender) get our payment in time.

We also have a surplus cash pooling mechanism. If a promoter has five different projects in five different states and we have funded more than one of them, we have a pooling mechanism so that in case there is a deficit in one project, the surplus of the other projects could be utilised to pay the debt service (i.e. principal + interest) of this account. It is a firm contractual arrangement and not an informal arrangement.

We are also the only lender who has, in recent years, been connecting the software of our company to that of the solar plant so that we can get minute-by-minute updates, i.e., “real-time monitoring” in respect of generation and performance of the equipment. Normally lenders refer to audited statements which are obtained 3-6 months after the end of the quarter or year – this cannot be “early warning” as the data is received late. Our online assessment tracks projects and equipment on a minute-by-minute basis so as to provide us “early warning” signals of anything going wrong in the project.

“Fastag” data i.e., data on electronic toll collection for roads has really revolutionised monitoring aspect of project finance to the sector. Earlier there used to be a worry that some of the cash collected at tollbooths, may be syphoned out prior to deposit in the escrow account on which lenders have a charge. After implementation of “Fastag”, on PPP projects in national highways, this risk is almost eliminated because the toll collection comes directly to the escrow account. NHAI proactively provides data on “Fastag” toll collection, enabling lenders like us to monitor our projects more effectively.

In the last 10 years, there has been tremendous improvement in infrastructure projects. What has changed and how are you as a

lender impacted?

The changes have been largely positive. First the nature of risk sharing in concession agreements and other PPP contracts, has significantly improved. For example, in roads, earlier the amount of land NHAI used to acquire was 80 per cent or less before the promoter could start construction work on the project. Now NHAI acquires a substantially larger share of land prior to handing it over to the promoter.

In the case of solar parks (there are several in the country), land required for the project, is acquired by the government. Utilities/ water etc, are made available at the solar park. The private sector promoter/developer has to only set up his plant – it becomes a sort of “plug and play” model, thereby reducing risk substantially. In hybrid annuity projects, the government infuses a larger amount of money into the project so that it can be a stakeholder. Provisions of the concession agreement also protect projects from inflation and provides a cushion against certain types of interest rate changes.

Further, more and more projects have off-takers which are central government entities like Solar Energy Corporation of India (SECI), National Thermal Power Corporation (NTPC) etc as against state government owned power distribution companies (called “discoms”). Today in 60 per cent of solar and wind projects, the off-taker is a financially strong, central government owned entity.

In the last four years, the Insolvency & Bankruptcy Code (IBC) has improved recovery prospects as compared to the earlier system, in which it took about 10 years and after that too, it was unclear whether recovery would be possible. IBC does not mean that 100 per cent money is recovered if things go wrong – but it does give greater confidence in the recovery process as well as its timelines.

Infrastructure Investment Trusts (InvITs) and a few other structures have low leverage for projects as mandated by law/regulation, leading to a higher level of sustainability for such projects. Around 18-20 registered InvITs managed an aggregate AUM (assets under management) of around Rs.1.75 trillion by

FY 2023.

Data from rating agencies shows that the average rating in 2017 for bond issuances by infrastructure companies was in the BBB grade but today the average rating has improved to A+. These are fairly positive statistics and for investors like pension, provident and insurance funds – data indicates that infrastructure projects have a long tenor, better risk and recovery profile than industrial projects.

They are also expected to have a larger market in future, given the government’s National Monetisation Pipeline. It does not mean that the entire estimated amount would translate to business, but at least it means that the government has had a hard look at it and even if 70-80 per cent of the target is met, it will lead to a huge incremental market of viable infrastructure projects in the country.

Overall trends for projects, as per various parameters, have been more positive over the years. In solar power, for instance, in 2011-12, the tenor for loans provided by lenders for projects, was between 12-15 years.

Today lenders offer loan tenors of 20-22 years. Secondly, in 2011-12, the interest rates for solar power projects (the sector was considered to have significant risk), was 12-13 per cent.

Today the interest rate has come down to 8.5-9.5 per cent. Third, the debt equity for such projects, in 2011-12, was 70:30, today it is 80:20, indicating a higher degree of comfort of lenders to such projects in view of, among other things, stabilised technology. Earlier only floating rate debt was given, today lenders like NIIF IFL are offering fixed rates whereby the interest rate risk of the project is eliminated. Fourth - earlier these projects were not bid out; they were allocated by the government and had subsidies in the form of “feed-in tariffs”, but now there are competitive transparent bids. Fifth - because of the solar panel prices falling internationally, solar power tariffs have also fallen from Rs.15 per unit (kwh) in 2011-12 to around Rs.2.5 to 3.5 per unit in recent years. Capital cost has fallen from Rs.15 million per MW (megawatt) to around Rs.3-4 million

per MW.

What is the return that investors get in infrastructure lending and why is it such a hot thing for the global markets?

Let me give an example of NIIF IFL i.e. current and potential returns to equity investors in this business. In NIIF IFL, because we finance low-risk operational projects, the spread (i.e. the difference between the lending rate and the borrowing cost) is lower. This follows the universal rule in finance – “low-risk, low-return”. For NIIF IFL, the spread is low, at around

1.2 per cent. This translates to a net interest margin (NIM) of 2.4-2.5 per cent, at our level of leverage. Since we operate out of only one office and have only about 50 employees, the operational expenses are extremely low at

0.3 per cent (i.e. percent of average assets).

Since there are zero per cent Non-Performing Assets (NPAs), technically the credit cost is zero. However, the RBI still mandates some amount to be set aside even for standard (i.e. performing) assets. Therefore, our credit cost (i.e. provisioning) is around 0.3-0.4 per cent. NIIF IFL is exempt from corporate income tax. Therefore, the return on asset (RoA) is 2.5 per cent - 0.3 per cent - 0.3 per cent = 1.9 per cent. At peak leverage of 8-9x permitted by rating agencies (since our portfolio is diversified, sufficiently “seasoned” and low-risk in nature), technically the return on equity (RoE) would be ~16-17 per cent. RoE would be lower till the company reaches peak leverage, which could happen in 1-2 years from now.

As against the above, in general, lenders with a large percentage of NPAs can never cross

8-9 per cent of return on equity. Maintaining asset quality is the key to higher RoEs in the infra lending business.

Does this bring down the cost

of borrowing?

The cost of borrowing is dependent on market conditions; movement of risk-free government securities or G-sec (i.e. representing interest rate risk) as well as how the market perceives any individual lender’s risk level (represented by “spread” over G-sec). Today we borrow at about 70 basis points above G-sec, which is very competitive among peers. The key factors for lower cost of borrowing include market perception of (i) ownership, quality of management & corporate governance (ii) asset quality, diversification, ALM, process, systems etc (iii) quality of people, at all levels (iv) clear strategic thought and focus (v) profitability

Though NIIF IFL has indirect equity investment from the Government of India, we are not a public sector entity; for example, we have no government nominee on the board. So, profitability and return are more comparable to a private sector lender.

How do you see the infra market shaping up in the next five years?

In roads the government has a huge plan and have announced that more and more projects would be in the PPP mode. They are also planning a large number of TOT, hybrid annuity (HAM) and Build-Operate-Transfer (BOT), to increase. So, in the road sector, there is a good scope.

There was uncertainty in ports till 1-2 years back. But the government brought in new legislation which clarifies the extent of freedom for each major port to price and run their business. After this legislation, the optimism in the port sector is high.

On airports - this government has been focussing not only on the large airports but also about 100-150 smaller airports. While many of them are not yet in the PPP mode and do not have private sector management, this is expected to happen in the next 1-2 years.

In transportation, roads, ports and airports have an extremely high probability of expansion of the market. In terms of railways, there are a number of metro rail projects in the country, of which 30-40 per cent are in the private sector. So, roads, ports, airports, metro rail and certain areas of railways, are expected to move to the PPP mode in a very large way, giving an opportunity for both private entrepreneurs in terms of equity investment as also in terms of additional opportunities to lenders.

In terms of energy, green hydrogen projects are still some time away and with respect to commercial viability. In terms of power generation, there is a huge existing market with respect to solar and wind power projects. These are also expected to be accompanied by storage projects. There are also combined generation and storage projects coming up. Viable projects under “pumped hydro” represents a relatively new prospect for lenders. (Pumped hydro represents two water reservoirs at different elevations that can generate power as water moves down from one to the other and is pumped back to the one at a higher elevation).

If India is going to get so much additional power generation, transmission networks are also required to transmit the generated power from one place to another. Transmission projects in the private or PPP projects are extremely safe. Once they are constructed, they are almost like annuity projects, with predictable cash flow and relatively low cost of maintenance. By and large, the off-taker for such projects, the Power Grid Corporation of India (PGCIL), has a good track record in terms of payment, AAA credit rating, is the nodal agency of the Government of India in respect of transmission.

There is less scope in oil and gas pipelines. This subsector is not going as well as was originally anticipated, in the context of PPP/ private sector projects. A smaller market could be water and sanitation including solid waste management, water supply, desalination plants and projects in the PPP mode including under the Namami Gange initiative of the Government of India.

In the communication sector, there are

two to three emerging technologies associated with telecom towers in the context of, for example, providing/ enhancing coverage and connectivity within large buildings such as malls. Data centres as well as “data centre interconnect” also represent a potentially large emerging opportunity.

In social and commercial infrastructure, hospitals, educational institutions, hotels and industrial parks are key growth categories.

In urban infrastructure projects, the key risk is off-taker risk, especially where municipalities are the off-takers. There are 7-8 municipalities that have a good track record of payment and thereby a good credit rating. There are roughly 40 of them which are in “A” or above category and very few in the “AA” or above category.

Waste segregation is not practiced in many parts of the country. Given this, waste-to-energy projects have faced issues relating to the quality of inputs/fuel. Some of them are based on emerging technologies, not yet established enough to give comfort to lenders.

How do you ensure ESG compliance in projects that you fund?

We have a separate ESG team, uniquely qualified and experienced in this area.

Coal based power projects are outside our ambit, even though they can be profitable. Normally environmental risk assessment by most lenders in India, is limited to checking compliance with pollution control board (PCB) norms. NIIF IFL goes a step further and also monitors areas like ground water usage. Solar projects are encouraged to go for robotic cleaning to conserve water. We have covenants in loan agreements relating to installation of bird diverters (for example, which enables safety of birds in projects with high tension transmission lines) and lightning arrestors (which protects the principal project area from lightening).

In the interest of sustainability in solar power projects, we are encouraging bifacial modules - where one side receives direct sunlight and the other receives reflected sunlight. This increases efficiency, pushes up generation and results in greater revenue and financial sustainability.

In case of certain types of solar projects, we have conditions in loan agreements mandating methods of safe disposal of panels so as to ensure that there is no contamination due to improper disposal of panels.

In order to ensure compliance with ESG conditions in loan agreements, NIIF IFL

also stipulates penalties for non-compliance with key terms.

- E Jayashree Kurup